135 Maps

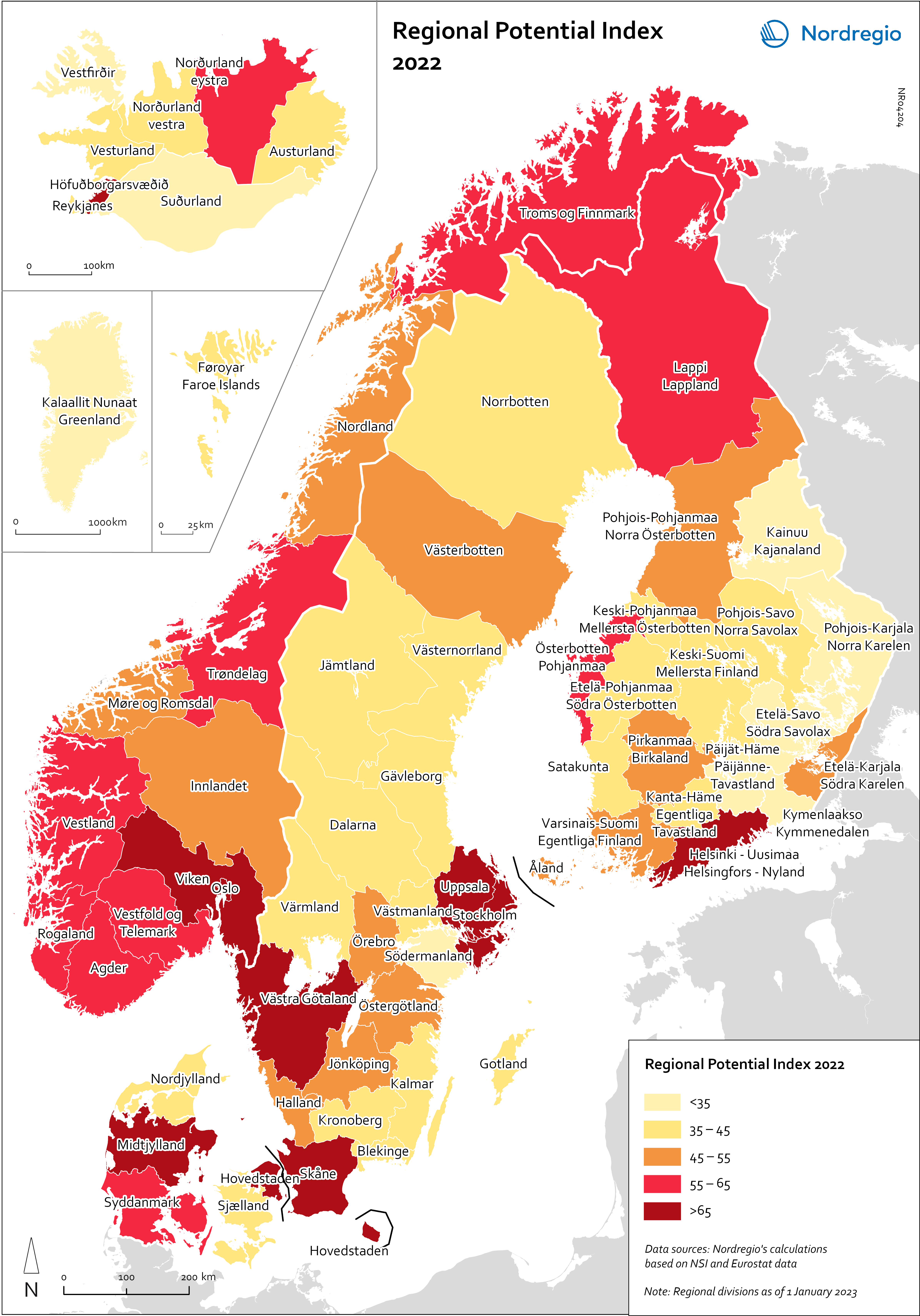

Regional Potential Index 2022

This map shows the result of Nordregio’s Regional Potential Index in 2024 (data from 2022). Nordregio’s Regional Potential Index (RPI) enables cross-regional comparison of development potential and illustrates the regional balance between the Nordic countries and has been part of the State of the Nordic Region report since 2018. The purpose of this multidimensional index is to summarise the current and past performance of the Nordic regions across major policy domains. The index helps to identify regions that have high potential and those in need of further support to boost their potential and meet existing challenges. It provides policy-makers with a comparative learning tool that informs the design of effective regional development strategies at Nordic level. Nordregio’s RPI is a multi-item measurement scale that incorporates information about the demographics, labour market and economic output of the Nordic countries’ 66 administrative regions. It consists of eight indicators classified into four main groups and eight subgroups. These components and indicators were originally selected on the basis of their relevance for regional development. The 2024 RPI is based on a new refined method that maintains a similar set of indicators but applies a more robust statistical process to the construction of the RPI. In brief, the new methodology consists of a pre-processing stage, in which the input data is prepared for analysis, and a processing stage, in which the indicators are weighted and aggregated. More information about the method can be found in the State of the Nordic Region 2024 report. The RPI was calculated retroactively for the 2015–2023 period. However, the focus in this section is on 2022 – the most recent year in our time series with full data coverage. The map shows the redesigned RPI for that period. In line with the principles of accumulation and agglomeration that drive the…

2025 April

2025 April - Demography

- Economy

- Labour force

- Nordic Region

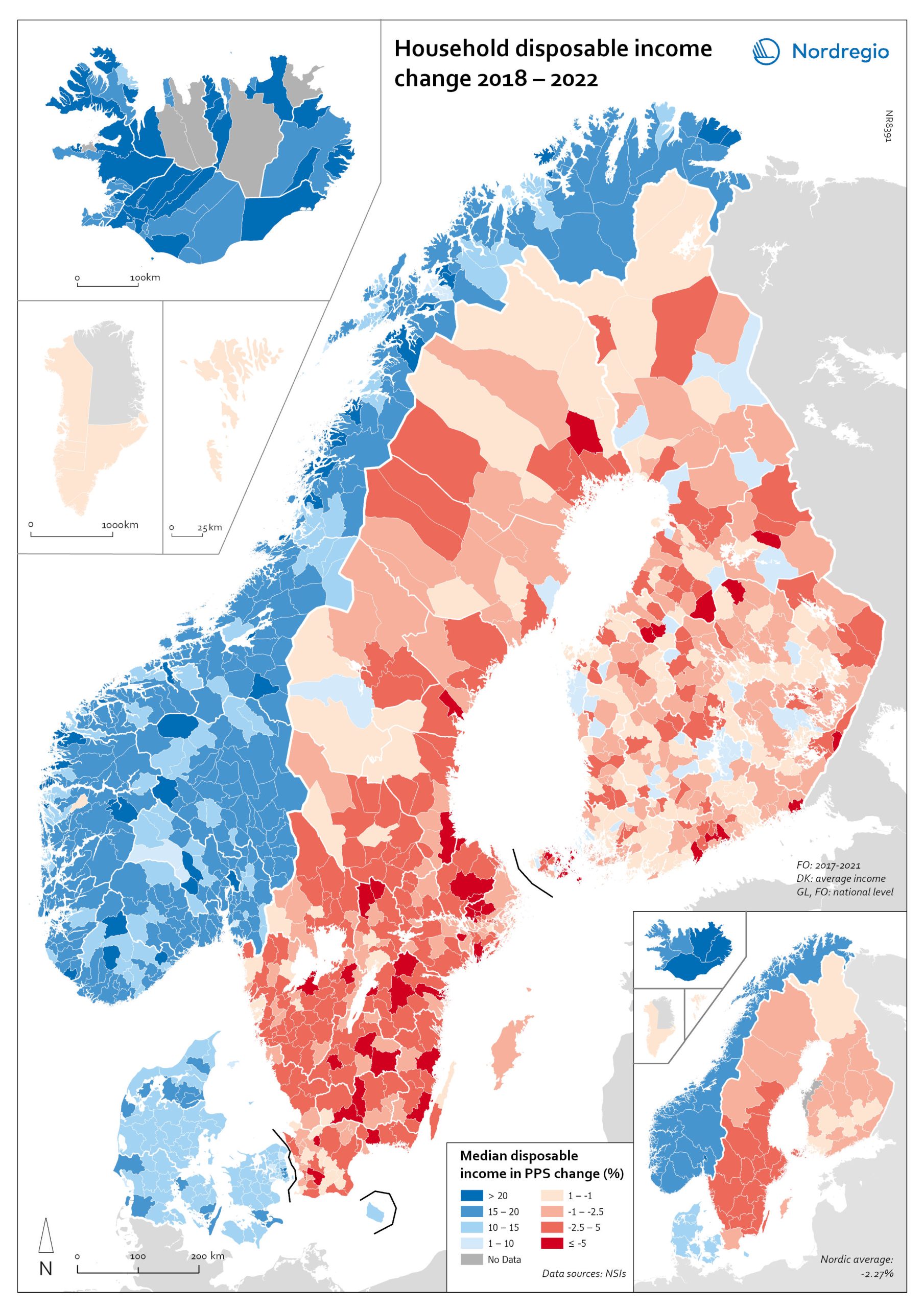

Household disposable income change 2018-2022

This map shows the percentage change in household disposable income between 2018 and 2022 in Nordic municipalities (big map) and regions (small map). Household disposable income per capita is a common indicator of the affluence of households and, therefore, of the material quality of life. It reflects the income generated by production, measured as GDP that remains in the regions and is financially available to households, excluding those parts of GDP retained by corporations and government. In sum, household disposable income is what households have available for spending and saving after taxes and transfers. It is ‘equivalised’ – adjusted for household size and composition – to enable comparison across all households. Purchasing Power Standards (PPS) is used to compare the countries’ economies and the cost of living for households. As shown in the map, between 2018 and 2022, household disposable income increased for all Danish, Icelandic, and Norwegian municipalities and decreased for Finnish and Swedish municipalities. On average, the city municipalities have higher incomes and increased most in Finland and Sweden in 2018–2022. In Sweden, a tendency towards larger falls in income was observed in several southern municipalities. In summary, absolute household income increased in all Nordic countries but not when measured in purchasing power. Based on this metric, on average, Norwegian households are the most well-off and Iceland the worst off, while Danish households benefited from a stronger currency in 2022. Single-parent households have had lower increases in household income than other families in Norway and parts of Sweden. Municipalities show a similar trend in Norway and Denmark, although Norwegian coastal municipalities fared slightly better in 2022. Disposable income is falling in all Swedish and Finnish municipalities.

- 2025 April

- Economy

- Nordic Region

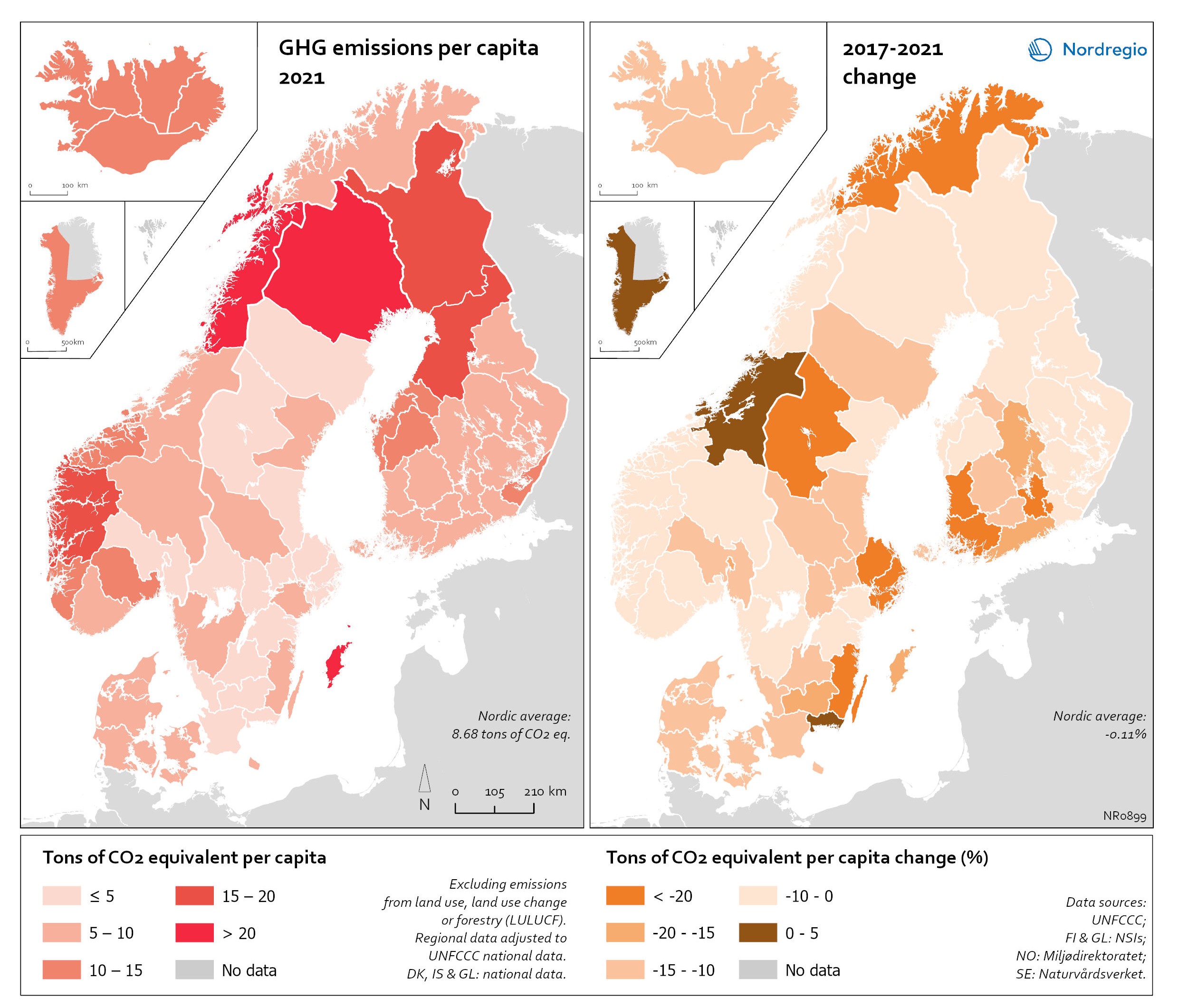

Regional GHG emissions per capita in 2021 and change 2017-2021 on a territorial basis

The data excludes emissions from land use, land use change or forestry (LULUCF). The regional data has been adjusted to UNFCCC national data. The data for Denmark, Iceland and Greenland is on national level. It should be noted that displaying emissions on a territorial basis may be skewed due to the inter-regional dynamics of energy processes, natural resource distributions and concentrations of industrial activities. From 2017 to 2021, the Nordic regions cut their per-capita GHG emissions by on average 11.3%, with an overall Nordic average fall of 8.7% over the same period. In regions historically reliant on fossil fuels for heat and power generation, emissions have continued to decline. This trend is evident in Denmark, as well as in Southern Sweden and Southern Finland – densely populated areas that have taken steps toward expanding district heating coverage and reducing carbon intensity. The largest decrease in GHG emissions per capita was found in Troms and Finnmark, with a 42.3% decrease, Satakunta with a 30.2% decrease and Päijät-Häme – Päijänne-Tavastland with a 29.2% decrease. Only three regions (Greenland, Trøndelag and Blekinge) saw an increase in GHG emissions per capita. At an aggregated level, industrial-related emissions decreased throughout the Nordic Region, but this trend does not hold true for regions in Norway with intensive offshore oil and gas operations. For instance, Nordland, Vestland, Møre og Romsdal, Vestfold and Telemark exhibited the highest per capita emissions in 2021. Between 2017 and 2021, emissions were increasing in many Norwegian regions with intensive offshore oil and gas activity, but also in Norrbotten in Sweden (21.2 tonnes of CO2 equivalent per capita) and Gotland (33.6 tonnes of CO2 equivalent per capita) due to intensive activity in the metal and cement industries, respectively, as well as in several Finnish regions. At the other end of the scale, the…

- 2025 April

- Environment

- Nordic Region

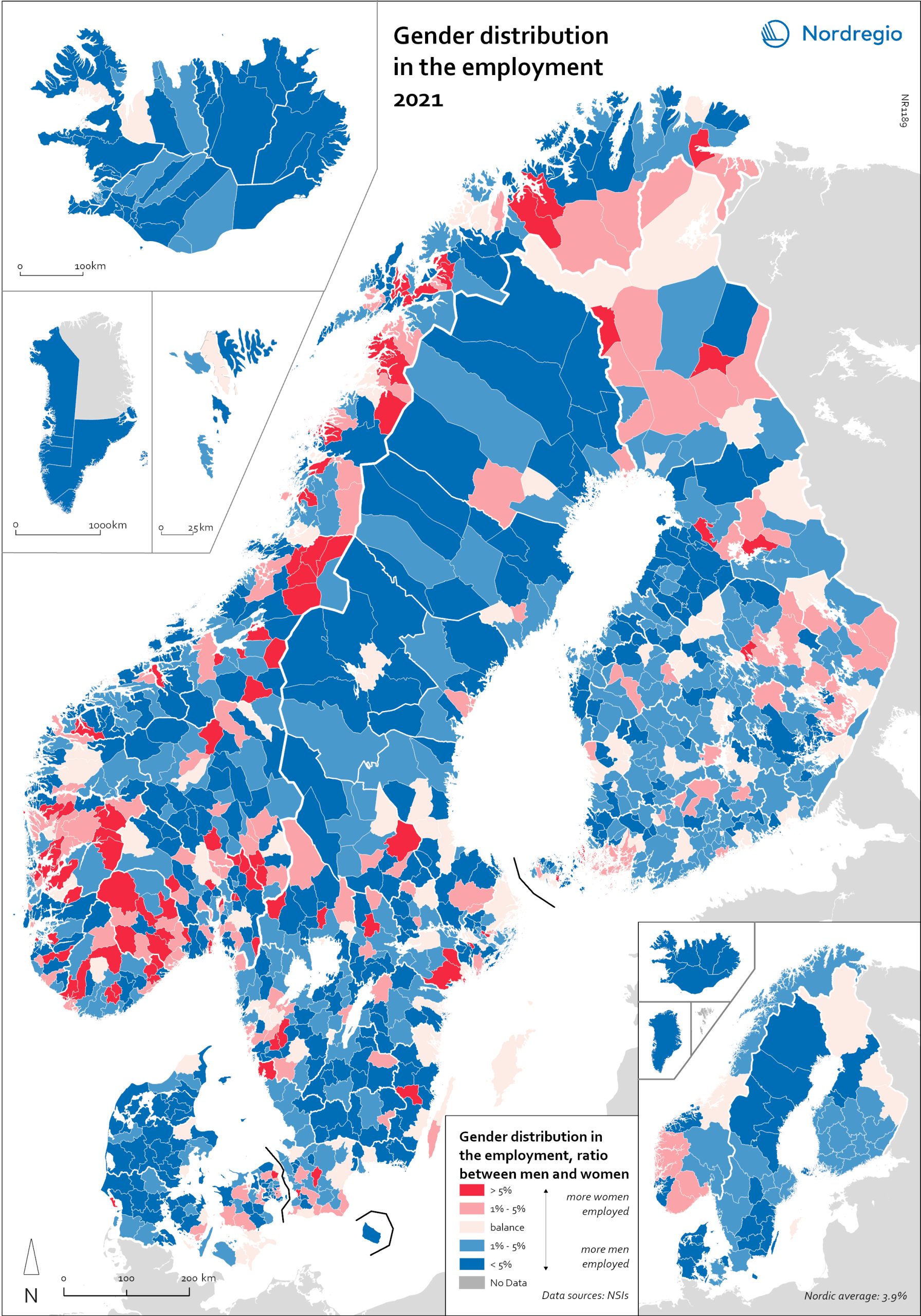

Gender distribution in employment 2021

This maps shows the gender distribution in employment at both municipal (big map) and regional levels (small map) in the Nordic Region in 2021 (measured in November). Blue shades indicate more men employed and red shades more women. Most regions had higher employment rates for men than women, with an average of 3.7% more men across the countries and sectors. In Finland, the rates were more balanced, with only 1.3% more men in employment. In three regions in Finland, employment rates were slightly higher for women: Etelä-Karjala – Södra Karelen, with 0.8% more women than men; Kainuu – Kajanaland, with 0.4%; and Uusimaa – Nyland with 0.1%. These are the only regions in the Nordic countries with a prevalence of employed women at the regional level. For the rest, employment rates were higher for men, with Icelandic regions having the largest share: Suðurnes had 11.3% more men than women, Vesturland 8.8%, Austurland 8.7%, and Suðurland 8.2%. The average for the Icelandic regions was 7.5%. For Denmark, this was 4.9%, for Sweden, 3.9%, and for Norway, 3.4%. At the municipal level, however, the situation was much more varied. Åland is one of the most extreme examples. Although the average was 2.5% more men employed than women, Åland has several municipalities with extremes at both ends. On the one hand, there are municipalities like Lumparland, with 16% more women than men, and Brändö, with 11.3%. On the other hand, Kökar had 64% more men than women. The variations between Ålandic municipalities can largely be attributed to the municipalities’ population size. The larger cities, like Trøndelag in Norway, may be more balanced at the regional level, but within the region, there are municipalities with a 20% prevalence of women in employment (Namsskogan, Meråker, Holtålen), as well as some with 18% (or higher) more…

- 2025 April

- Economy

- Labour force

- Nordic Region

Gini coefficient change 2018-2022

This map shows the percentage change in the Gini coefficient between 2018 and 2022. The big map shows the change on municipal level and the big map at regional level. Blue shades indicate a decrease in income inequality, while red areas indicate an increase in income inequality The Gini coefficient index is one of the most widely used inequality measures. The index ranges from 0–1, where 0 indicates a society where everyone receives the same income, and 1 is the highest level of inequality, where one individual or group possesses all the resources in the society, and the rest of the population has nothing. The map illustrates significant variations in the change in income inequality across Nordic municipalities and regions. Between 2018 and 2022, income inequality increased in predominantly rural municipalities, notably in Jämtland, Gävleborg, Dalarna and Västerbotten in Sweden, as well as Telemark in Norway. For Denmark, the rise in inequality is mainly for the municipalities in Western Jutland. At the same time, approximately one third of municipalities in the Nordic Region experienced a decrease in income inequality during the same period, primarily in Finland and Åland. For example, in Finland, the distribution of inequality was more varied. This trend aligns with the ongoing narrowing of the household income gap observed in many Finnish municipalities since 2011, which is mainly attributed to the economic downturn of the early 2010s, as well as demographic shifts such as outmigration and ageing.

- 2025 April

- Economy

- Nordic Region

Electricity production 2021

This map shows the spatial distribution of Nordic electricity production per capita, by volume and source type in the Nordic Region in 2021. The data is presented at a regional level, except for Iceland (national level) and Denmark (bidding zones). The circles represent electricity production in GWh, while the green shades indicate electricity production per capita (kWh). Finally, the colour of the circles denotes the source of electricity. The Nordic Region overall has a high electricity production per capita; in fact, Iceland and Norway have the world’s highest electricity production per capita. The electricity mix in 2021 was 96% fossil-free – 73% from renewables (mainly hydropower) and 17% from nuclear power. In 2000 85% of the electricity production was fossile-free. Still there are clear spatial differences in the electricity production. Firstly, we see the high amount of electricity being produced for the five nuclear facilities in Sweden and Finland. Secondly, a substantial volume of hydro-electricity is produced in southern Norway, throughout Iceland, Northern Sweden and Northern Finland. As a result, over half of Nordic electricity is produced from hydropower. Wind power is the source of electricity that has been growing the most during the last two decades, from 1.2% in 2000 to 14% in 2021. The regions with the highest electricity production per capita are in Iceland, Northern Sweden, and Northern and Western Norway. Both Finland and Denmark are net importers of electricity, but both countries have rapidly transitioned away from fossil fuels. Cheap and fossil-free electricity is a prerequisite for the green transition and with growing industries within e.g. battery production, green steel and mining, the need for fossil-free electricity is expected to increase in the coming decades.

- 2025 April

- Environment

- Labour force

- Nordic Region

Greenhouse gas emissions intensity of employment in 2022

This map shows the tonnes of greenhouse gas emissions per person employed in Nordic municipalities (big map) and regions (small map) in 2022. The data for Iceland is presented at the national level, while no data was available for the Faroe Islands and Greenland. The map is based on data on emissions per sector and country from Eurostat and detailed employment by sector data from the Nordic statistical offices. By calculating the average emissions per person employed and per sector we could use municipal employment by sector data to assess the average emissions per person employed in each municipality. The results are an estimation based on the assumption that all jobs in the same sector have the same GHG emissions. In 2022, greenhouse gas (GHG) emissions per person employed in the Nordic Region were 15.7 tonnes. This is higher than the EU average of 13.5 tonnes. There are also fairly big differences between the Nordic countries, with higher emissions per person employed in Iceland (28.6), Denmark (23.1) and Norway (20.5) and lower emissions in Finland (15.7) and Sweden (8). On the other hand, the emissions per person employed have decreased faster in the Nordic Region than for the EU as a whole. In the last decade, emissions per person employed fell by 24% in the Nordic Region compared to the EU average of 22%. The biggest decrease (32%) was in Finland. The sectors with the highest emissions per worker vary slightly between the countries. In Sweden and Norway, the sector with by far the highest emissions per worker was the manufacture of petroleum coke and refined petroleum products. However, it should be noted that the number of workers in this sector is small. In Denmark, the highest emissions by person employed could be found in water transport; in Finland, in…

- 2025 April

- Environment

- Labour force

- Nordic Region

Tertiary education attainment level 2022

This map shows the share of people aged 25-64 years with a tertiary education in Nordic municipalities (big map) and regions (small map) in 2022. All of the Nordic countries have a higher share of people who completed tertiary education than the EU average. The highest share is in Sweden (48.6%), followed by Norway (47.8%), Iceland (42.9%), Finland (42.7%) and Denmark (42.1%). There are, however, big differences within the countries with a considerable urban-rural divide in terms of tertiary education. The capital regions of Oslo (66%), Stockholm (58%), Copenhagen (Hovestaden) (51%), Reykjavik (51%) and Helsinki (Uusimaa) (49%) stand out with particular high share of tertiary educated population. Conversely, rural regions such as Iceland outside of Reykjavik (30%), Kymenlaakso (34%), Kainuu (34%), Etelä-Savo (35%), Satakunta (35%) in Finland and Syddanmark (35%), Midtjylland (36%) and Nordjylland (36%) in Denmark are among the regions with the lowest share of tertiary educated population. The successful implementation of the Bologna Process and the derived increase in educational levels of young people in the Nordic Region coincides with large numbers of the ‘baby boomer’ generation leaving the labour market. This generation has a significantly lower level of education than the current 24–35 age group – i.e. those who are now entering the labour market. This trend can be seen across the Nordic Region.

- 2025 April

- Labour force

- Nordic Region

Employment in high-skilled occupations 2022

This map displays the share of high-skilled workers as a share of the total number of workers in Nordic municipalities (big map) and regions (small map). “High-skilled workers” is here defined as group 1-3 (Managers, Professionals and Techinicians/associated professionals) of the International Standard Classification of Occupations (ISCO). For Iceland national data is used. The EU average of high-skilled workers is 43%, and the Nordic countries are at the top of the rankings – 49.5% in Finland, 51.1% in Denmark, 54.2% in Norway, 54.5% in Iceland and 58.9% in Sweden. On a regional level, the highest share is in the capitals and bigger cities, such as Stockholm (72%), Oslo (71%), Hovedstaden (Copenhagen) (60%), Uppsala (60%) and Uusima (Helsinki) (59%). The lowest shares are in the Finnish regions of EteläPohjanmaa, Keski-Pohjanmaa, Satakunta and Etelä-Savo (less than 40%). However, this does not necessarily mean that employers will have a greater chance of successfully recruiting high-skilled workers in the future, partly because those in this group already have jobs and partly due to generally lower investments in education.

- 2025 April

- Labour force

- Nordic Region

- Research and innovation

Labour supply replacement 2023

This map shows the ratio between the age groups 20–29 and 55–64 at the municipal level (big map) and regional level (small map). A ratio below 1 indicates that fewer individuals are entering the labor market than leaving it, while a ratio above 1 means more people are entering than exiting. For the Nordic Region as a whole, the ratio is 0.95, meaning that there are slightly fewer people in the age group 20–29 than 55–64. Iceland is the only country with a ratio above 1 (Iceland: 1.3; Greenland: 0.99; Denmark: 0.97; Norway: 0.95; Finland: 0.94; Sweden: 0.93; Faroe Islands: 0.88; Åland: 0.63). All of the Icelandic regions, as well as the capital regions of Norway, Denmark and Finland, have a ratio above 1. In Sweden, the highest ratios are in Uppsala (1.25), Västerbotten (1.14) and Östergötland (1.03), while the ratio in Stockholm is below 1 (0.95). The lowest ratios are found in Etelä-Savo (0.62) and Åland (0.63) in Finland, Sjælland (0.63) in Denmark, Västernorrland (0.74) in Sweden, and in Vestfold og Telemark (0.78) and Viken (0.77) in Norway. However alarming these trends and developments are, they are neither new nor undescribed. An analysis of the factors and policy strategies that are influencing these developments enables adjustments to be made to future trends.

- 2025 April

- Demography

- Labour force

- Nordic Region

Working age population – 2023-2040 change

This map illustrates the projected change in the working-age population across Nordic municipalities (large map) and regions (small map) from 2023 to 2040. The working-age population is defined here as individuals aged 20 to 64. The blue areas on the maps represent municipalities and regions where the working-age population is expected to increase during this period. In contrast, the red areas indicate a projected decline in the working-age population. These projections are based on data from Nordic statistical institutes, though it’s important to note that the underlying assumptions may vary between Nordic countries. In most of the Western world, the working-age population is decreasing. In the EU, this age group is expected to decrease by 6.5% between 2023 and 2040. Only five EU countries – Malta, Luxembourg, Ireland, Sweden and Belgium – are expected to enjoy growth in the working-age population during this period. However, in the Nordic Region as a whole, the working-age population is expected to grow slightly, with an average increase of 1.9%. As the map shows, the distribution is quite varied, with considerable differences both between and within the countries. The biggest increase is expected in Iceland (28%), followed by Sweden (5.8%), Åland (3.9%) and Norway (0.6%). Decreases are expected in Finland (-0.5%), the Faroe Islands (-2.6%), Denmark (-3.2%) and Greenland (-11.4%). This development is in addition to the decreases already experienced by Finland since 2013. In general, the trend of growing populations in cities and decreasing populations in rural areas is expected to continue. The regions that are expected to have the highest working-age population growth include Höfuðborgarsvæðið in Iceland, Uppsala (+13%), Stockholm (+12%), Skåne (+9%), Halland (+7%) and Västra Götaland (+6%) in Sweden, Uusimaa (+8%) and Pirkanmaa (+5%) in Finland, and Oslo and Viken in Norway (+5%). In addition, Copenhagen municipality (+5%), Rødovre (+9%)…

- 2025 April

- Demography

- Labour force

- Nordic Region

Employment rate (55-74 years) 2022

This map shows the employment rate for the age group 55-74 years in the Nordic municipalities (big map) and regions (small map) in November 2022. Employment rate refers to the share of population in a particular age group that is in employment (LFS definition), in this map it is measured for the age group 55-74 years. Older adults (55+) were less affected by the pandemic. In general, this age group has a stronger attachment to the labour market, and a higher proportion work in occupations where remote work was possible. For quite some time, the Nordic Region has boasted a higher employment rate among older adult workers compared to the rest of Europe, although this gap has narrowed somewhat in recent years. In 2022, 75.5% of the Nordic population aged 55–64 were employed, whereas the EU average stood at 62.3%, representing a difference of 13 percentage points. In 2012, however, this difference was 21 percentage points, and in 2002, it was 29. The map shows variation between the Nordic countries, with Finland exhibiting a lower employment rate for this age group. The highest rates were observed in the Faroe Islands (62%), Greenland (61%), Åland (56%), and the Swedish regions of Jämtland-Härjedalen (55%) and Jönköping (54%). The Labour Force Survey (LFS) is the official source for labour market statistics and the only source that is comparable across countries. The data comes from a standardised survey that is conducted in the same way in all EU countries, as well as in many non-EU countries, including in Norway, Iceland and the Faroe Islands. The LFS is the main source for the map, however since it is not possible to break down at a municipal level, register data has been made to create estimates at a municipal level.

- 2025 April

- Labour force

- Nordic Region

Employment rate 2022 and Employment rate change 2020-2022 among foreign-born

These maps shows the employment rate in 2022 for those born in a EU country (top left) and those born outside of the EU (bottom left), as well as the change in employment rate between 2020 and 2022 for those born in the EU (upper right) and outside the EU (lower right). The data is displayed at NUTS 2 level and comes from the labour force survey (LFS). The category ‘foreign-born’ is quite heterogeneous and consists of everything from labour migrants to refugees – two groups who face quite different conditions and have different connections to the labour market. The employment rate for people born in another EU country – a group that includes a large proportion of labour migrants – has been on par with the employment rate for native-born people for a long time. As can be seen in the top-left figure in the map, in 2022 all NUTS2 regions except Southern Denmark had an employment rate of 75% or more for this group. The highest employment rate was observed in the Swedish NUTS2 regions of Middle Norrland, Stockholm and Western Sweden, followed by Oslo in Norway and Iceland. The employment rate for people born outside of the EU (a group that largely consists of refugees) has been lower for a long time than that of native-born people and those born in the EU. While the employment rate for people born in non-EU countries is still lower than for natives (a 15 percentage point difference (pp) in Sweden, 11 pp in Norway, 7 pp in Denmark and Finland, and 2 pp in Iceland), this gap has been closing in the last couple of years since the pandemic. Between 2020 and 2022, the employment rate for those born outside of the EU rose almost eight percentage points in Denmark…

- 2025 April

- Labour force

- Nordic Region

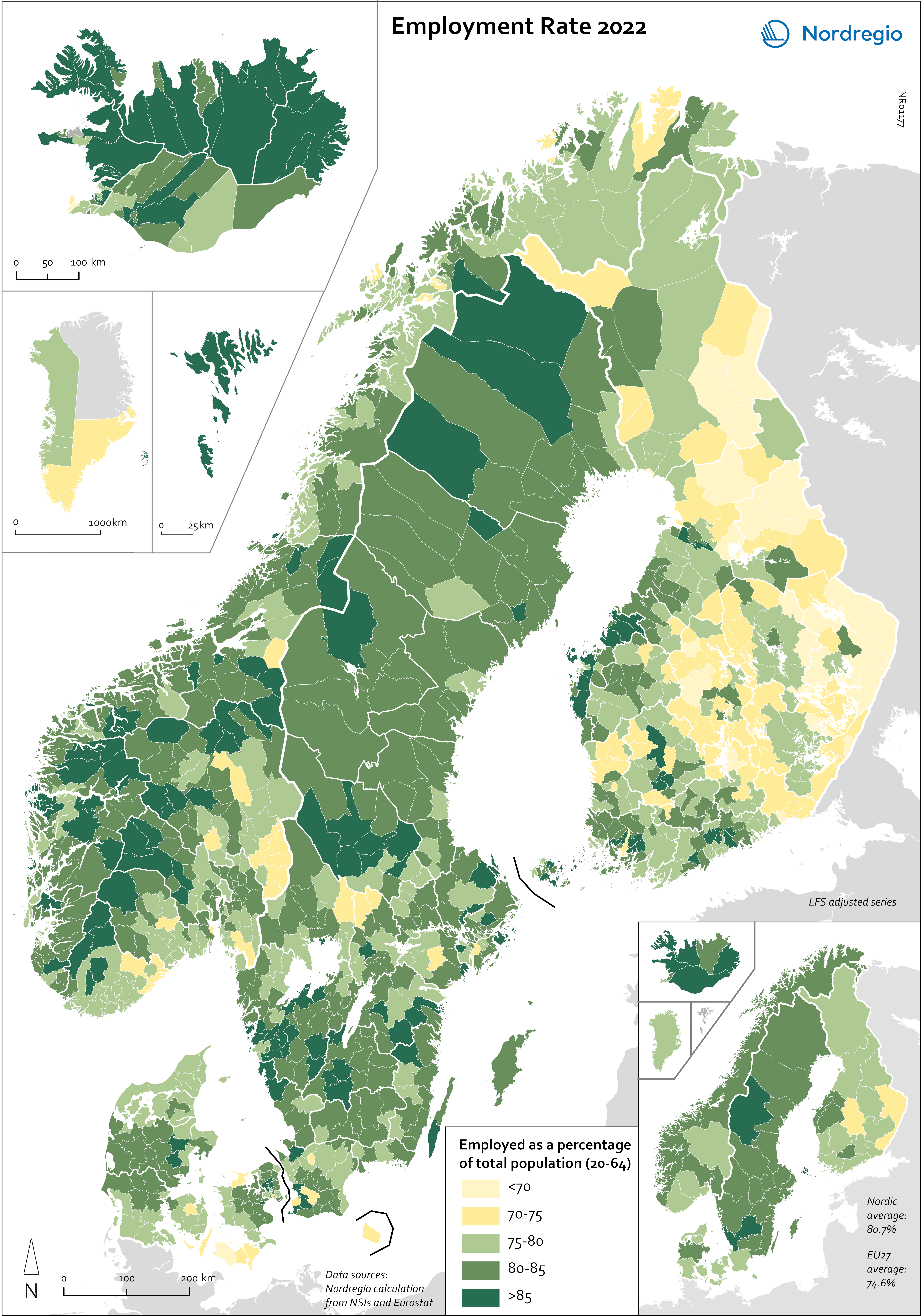

Employment rate 2022

This map shows the employment rate for Nordic municipalities (big map) and regions (small map) in 2022 (measured in November). Employment rate refers to the share of population in a particular age group that is in employment (LFS definition), in this map it is measured for the age group 20-64 years. At a national level, all of the Nordic countries have employment rates higher than the EU average (74.6%). The highest rates were in the Faroe Islands (93%), Åland (86%) and Iceland (83%), followed by Sweden (82.2%), Denmark (80.1%), Norway (80.9%), Finland (78.4%) and Greenland (75%). Of the EU countries, only the Netherlands (82.9%) had a higher employment rate than Sweden in 2022. As the map shows, most of the regions and municipalities had employment rates above 75% (the green areas on the map) in 2022, meaning that three-quarters of people aged 20–64 were working. In addition to the Faroe Islands, Iceland and Åland, the Swedish regions of Jämtland-Härjedalen, Halland and Jönköping also had employment rates of more than 85%. The only regions with employment rates under 75% were the Finnish regions of North and Southern Karelia and KeskiSuomi. On a municipal level, the highest employment rates were found in rural municipalities, mainly in Iceland and the Faroe Islands, as well as some municipalities in Österbotten in Finland (such as Pedersöe and Korsholm). Of the intermediate municipalities (between urban and rural), the highest employment rates were in the Swedish municipalities Habo (Jönköping), Hammarö (Värmland), Nykvarn (Stockholm), Gällivare (Norrbotten), Kungsbacka (Halland), Svedala (Skåne) and Mosfellsbær (Höfuðborgarsvæðið) in Iceland. Of the urban municipalities, the employment rate was highest in Garðabær and Kópavogur in the Capital Region of Iceland, Tyresö and Täby in the Stockholm region, Partille in Västra Götaland in Sweden, and Bærum and Rælingen in Viken in Norway. The lowest employment…

- 2025 April

- Labour force

- Nordic Region

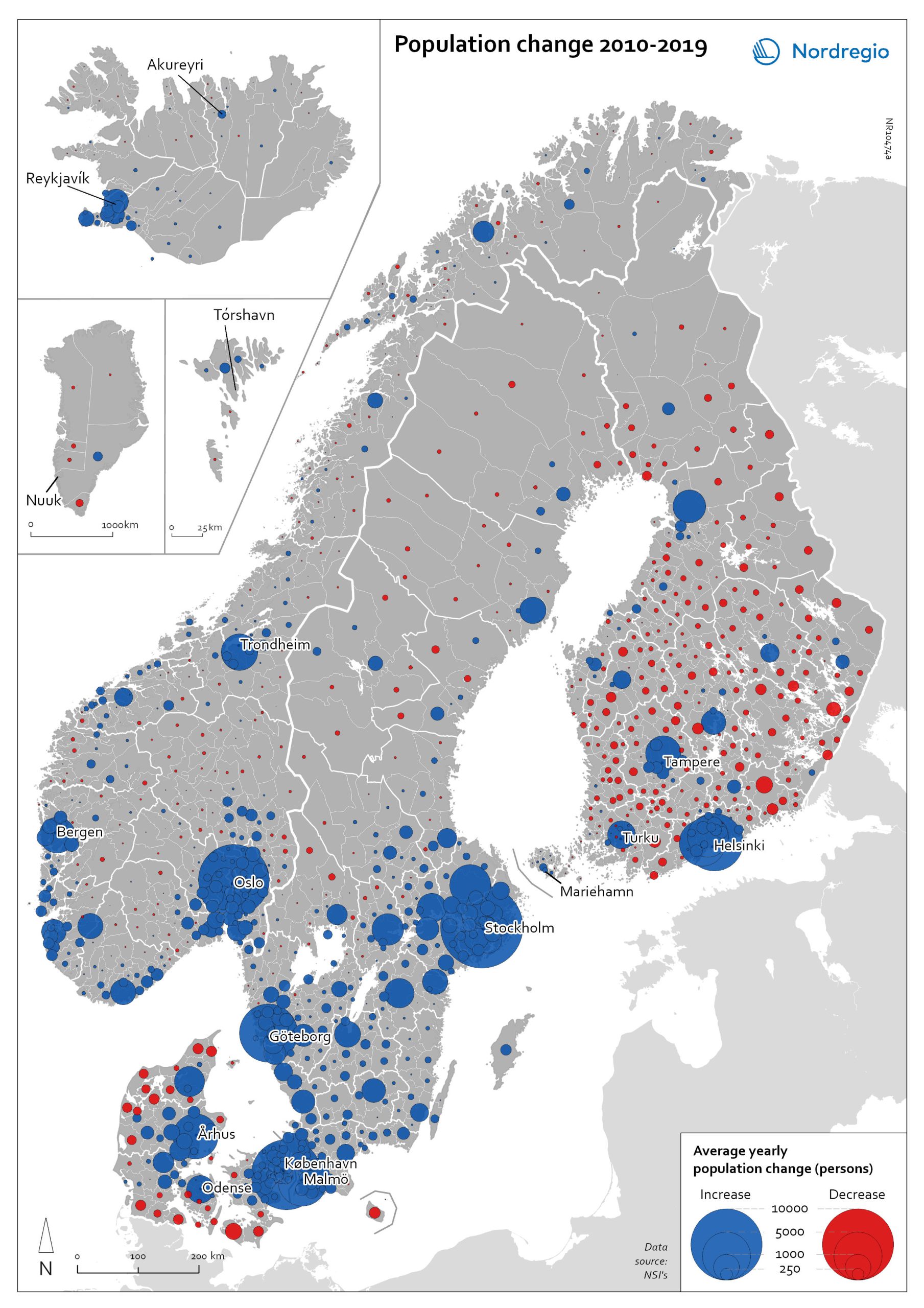

Population change 2010-2019

The map shows the type (positive or negative) and size of population change from 2010 to 2019 in all nordic municipalities. In Finland, Denmark, and Greenland there is a clear pattern of population growth in and around the larger cities and population decline in rural areas. Geographical and administrative differences mean that a much larger number of rural municipalities in Finland are dealing with population decline. Sweden experienced substantial population growth between 2010 and 2019, primarily due to high levels of international immigration. As a result, many rural areas also experienced population growth, particularly in the south of Sweden. However, in the more sparsely populated municipalities in the north of Sweden, the pattern is somewhat similar to that observed in Denmark and Finland, albeit with population decline in lower absolute numbers. Both Iceland and the Faroe Islands experienced substantial growth of their tourism industries within the period. This enabled some rural areas to maintain or even grow their populations. Norway exhibits more balanced population development in general, with a mix of population growth and decline in rural areas throughout the country.

- 2022 May

- Demography

- Migration

- Nordic Region

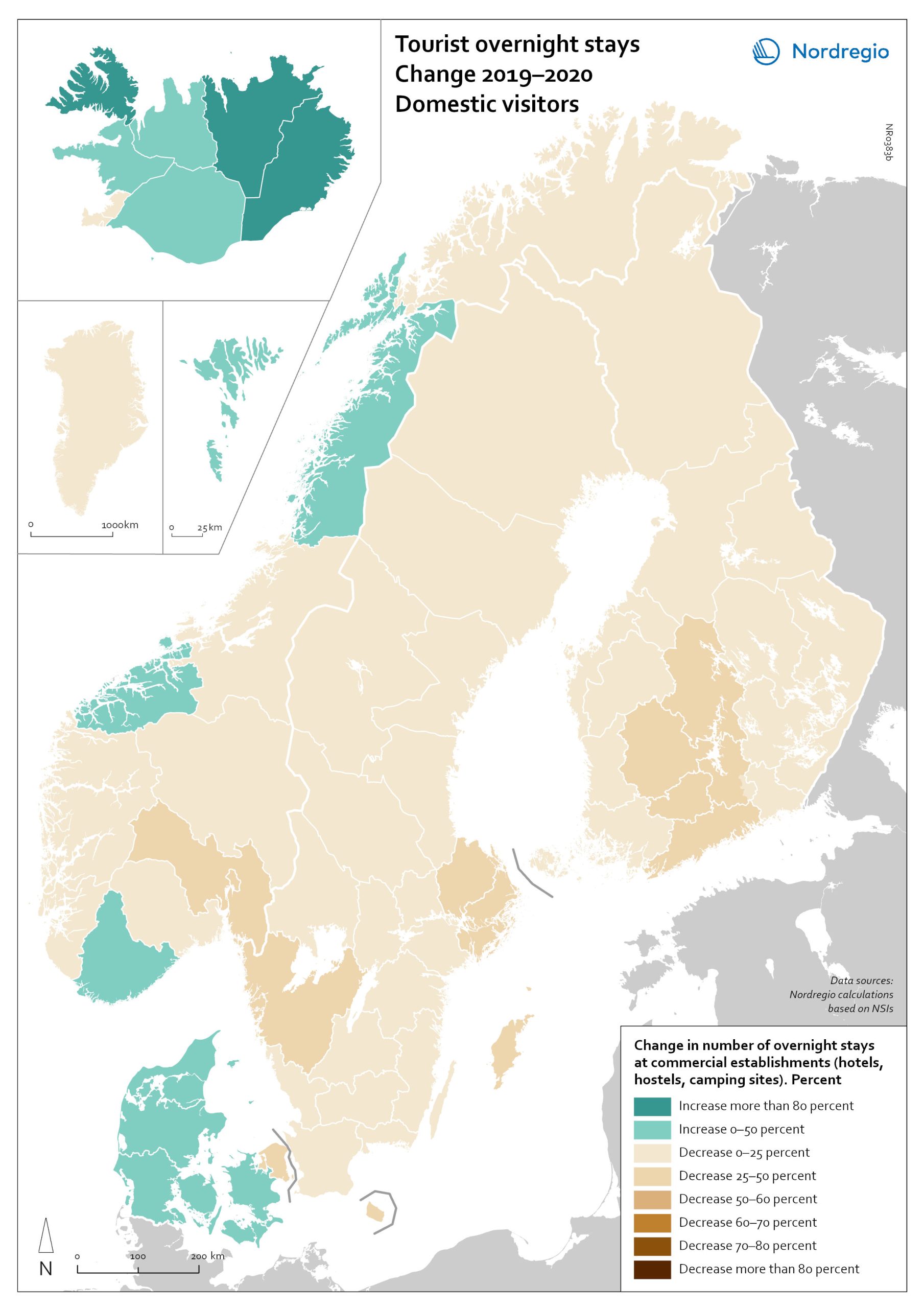

Change in overnight stays for domestic visitors 2019–2020

The map shows the relative change in the number of overnight stays at the regional level between 2019 and 2020 for domestic visitors. This map is related to the same map showing change in overnight stays for foreign visitors 2019–2020. The sharpest fall in visitors from abroad was in destinations where foreign tourists usually make up a high proportion of the total visitors. This is particularly relevant to islands like Åland (89% decrease on foreign visitors, from early 2019 to mid-2020) and to Iceland (66-77% drop depending on region). Lofoten and Nordland County in Norway, as well as Western Norway with Møre and Romsdal, which also have a high proportion of international tourists during the summer season due to their scenic landscape, also recorded sharp falls of 77-79% on foreign visitors during the same period. In Finland, the lake district (South Savo) and Southern Karelia, as well as the coastal Central Ostrobothnia (major cities Vasa and Karleby), recorded a 75-77% drop in the number of visitors from abroad. The fall here was mainly due to the lack of tourists from Russia. Even Finnish Lapland suffered a major fall in international visits during the winter peak period. For many local businesses that rely heavily on winter holidaymakers, the 2021/22 winter was a make-or-break season. In Sweden, the regions of Kalmar, Västra Götaland, Värmland and Örebro lost 77–79% of visitors from abroad, probably due to much fewer visitors from neighbouring Norway and from Denmark. In Denmark, the number of overnight stays by visitors from abroad to the Capital Region was down by 73%, whereas the number of domestic visitors declined by 27%. No region lost as many overnight visitors, both from abroad and domestic, as the capital cities and larger urban areas in the Nordic countries. Copenhagen, Oslo, Stockholm, Helsinki and Reykjavik…

- 2022 March

- Nordic Region

- Tourism

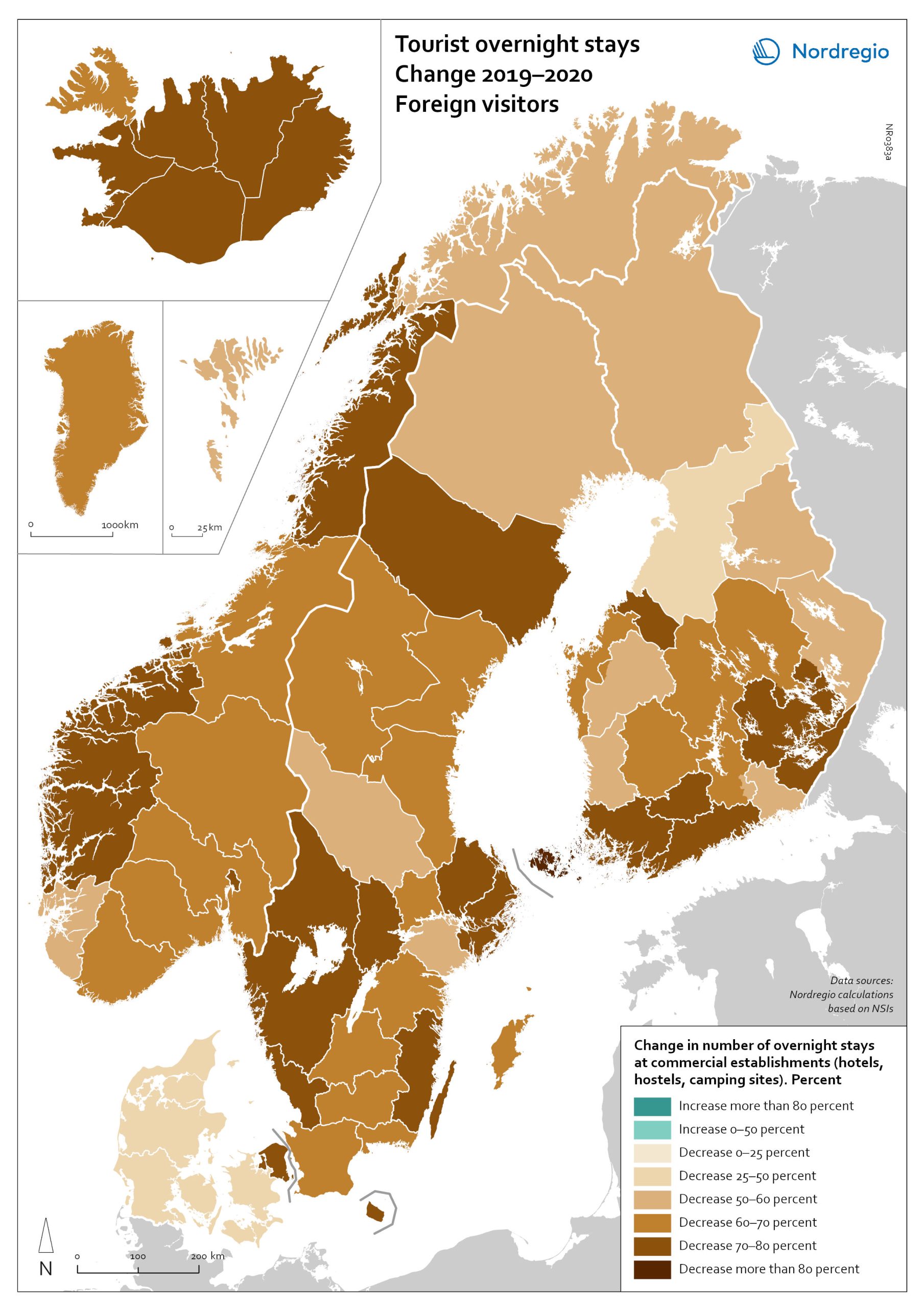

Change in overnight stays for foreign visitors 2019–2020

The map shows the relative change in the number of overnight stays at the regional level between 2019 and 2020 for foreign visitors. This map is related to the same map showing change in overnight stays for domestic visitors 2019–2020. The sharpest fall in visitors from abroad was in destinations where foreign tourists usually make up a high proportion of the total visitors. This is particularly relevant to islands like Åland (89% decrease on foreign visitors, from early 2019 to mid-2020) and to Iceland (66-77% drop depending on region). Lofoten and Nordland County in Norway, as well as Western Norway with Møre and Romsdal, which also have a high proportion of international tourists during the summer season due to their scenic landscape, also recorded sharp falls of 77-79% on foreign visitors during the same period. In Finland, the lake district (South Savo) and Southern Karelia, as well as the coastal Central Ostrobothnia (major cities Vasa and Karleby), recorded a 75-77% drop in the number of visitors from abroad. The fall here was mainly due to the lack of tourists from Russia. Even Finnish Lapland suffered a major fall in international visits during the winter peak period. For many local businesses that rely heavily on winter holidaymakers, the 2021/22 winter was a make-or-break season. In Sweden, the regions of Kalmar, Västra Götaland, Värmland and Örebro lost 77–79% of visitors from abroad, probably due to much fewer visitors from neighbouring Norway and from Denmark. In Denmark, the number of overnight stays by visitors from abroad to the Capital Region was down by 73%, whereas the number of domestic visitors declined by 27%. No region lost as many overnight visitors, both from abroad and domestic, as the capital cities and larger urban areas in the Nordic countries. Copenhagen, Oslo, Stockholm, Helsinki and Reykjavik…

- 2022 March

- Nordic Region

- Tourism

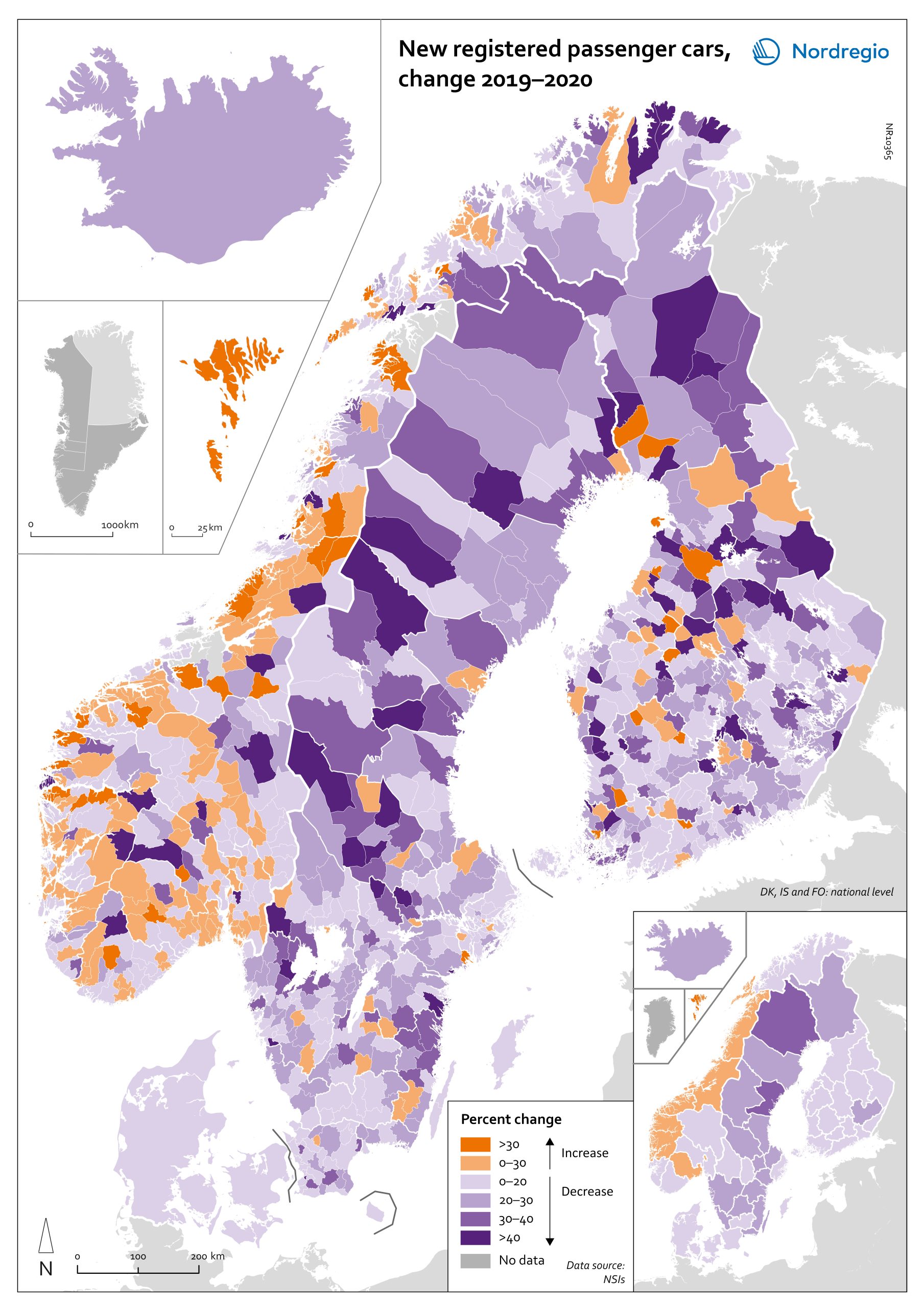

Change in new registered cars 2019-2020

The map shows the change in new registered passenger cars from 2019 to 2020. In most countries, the number of car registrations fell in 2020 compared to 2019. On a global scale, it is estimated that sales of motor vehicles fell by 14%. In the EU, passenger car registrations during the first three quarters of 2020 dropped by 28.8%. The recovery of consumption during Q4 2020 brought the total contraction for the year down to 23.7%, or 3 million fewer cars sold than in 2019. In the Nordic countries, consumer behaviour was consistent overall with the EU and the rest of the world. However, Iceland, Sweden, Finland, Åland, and Denmark recorded falls of 22%–11% – a far more severe decline than Norway, where the market only fell by 2.0%. The Faroe Islands was the only Nordic country to record more car registrations, up 15.8% in 2020 compared to 2019. In Finland, Iceland, Norway, and Sweden, there were differences in car registrations in different parts of the country. In Sweden and Finland, the position was more or less the same in the whole of the country, with only a few municipalities sticking out. In Finland and Sweden, net increases in car registrations were concentrated in rural areas, while in major urban areas, such as Uusimaa-Nyland in Finland and Västra Götaland and Stockholm in Sweden, car sales fell between 10%–22%. Net increases in Norway were recorded in many municipalities throughout the whole country in 2020 compared to 2019.

- 2022 March

- Economy

- Nordic Region

- Transport

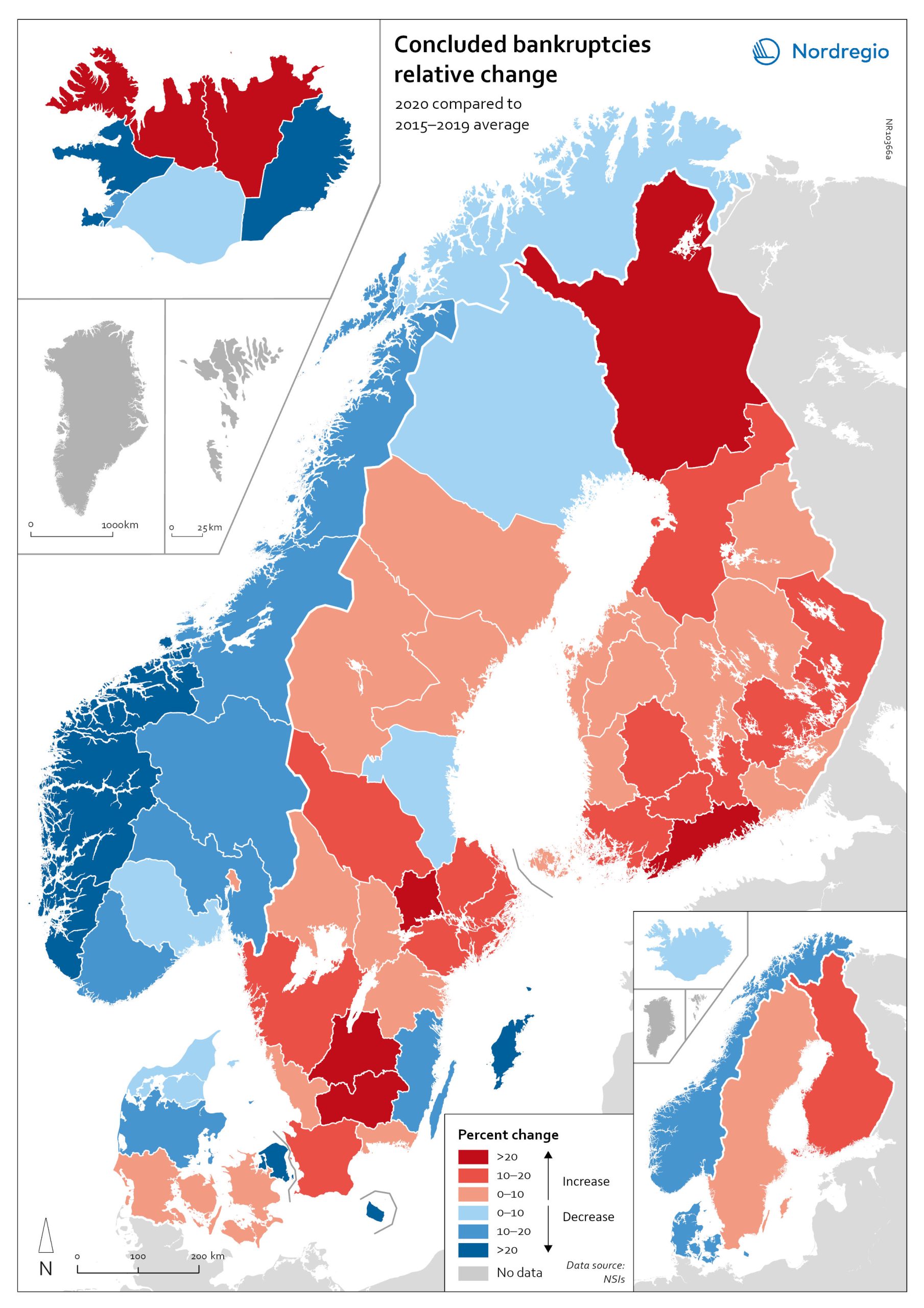

Relative change in the number of business bankruptcies

The map shows the relative change in the number of concluded business bankruptcies by region, 2015–2019 average compared to 2020. At sub-national levels, the distribution of business bankruptcies does not show a clear territorial pattern. In Iceland and Denmark, businesses in the most urbanised areas, including the capital regions, seem to have been those that benefited most from the economic mitigation measures (-23.9% in Höfuðborgarsvæðið and -24.4% in Region Hovedstaden). By contrast, Oslo is the only Norwegian region where there were more business bankruptcies in 2020 compared to the 2015–2019 baseline (1.9% increase). Most Norwegian regions did, in fact, have fewer bankruptcies in 2020, particularly in the western regions. One plausible explanation for this could be that the number of business failures during the baseline period was especially high in western Norway due to the fall in oil prices in 2014–2015. In Sweden the situation is even more mixed. Here, businesses in urban areas seem to have been more exposed to the distress caused by the Covid-19 pandemic. The most urbanised regions in the Stockholm-Gothenburg-Malmö corridor registered a greater increase in liquidations (Jönköping, Kronoberg and Södermanland regions saw surges of around 20%). However, predominantly rural regions in Sweden, such as Västerbotten and Jämtland, also recorded higher numbers of bankruptcies than average (9.8% and 8.8% increase, respectively). In Finland, the impact was greater in Lapland (26.9%) and around Helsinki (Uusimaa, 25.9%) than in the central parts of the country. Åland also experienced a moderate rise in business bankruptcies in 2020 (4.0%), mostly related to the tourism sector.

- 2022 March

- Economy

- Nordic Region

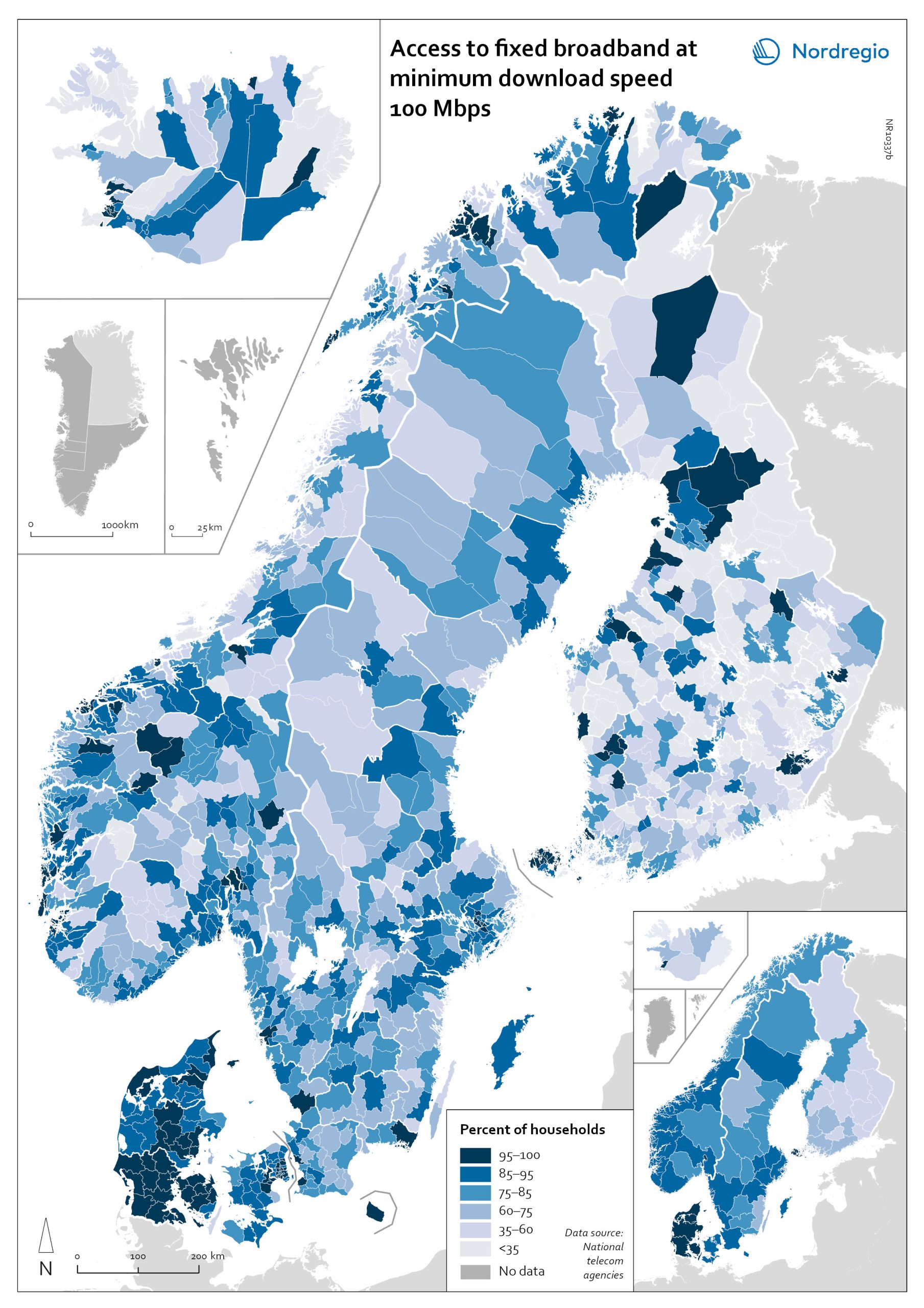

Access to fixed broadband at minimum download speed 100 Mpbs

The map shows the proportion of households that had access to fixed-line broadband with download speeds >100 Mbps (superfast broadband) at the municipal level, with darker colours indicating higher coverage. Overall, Denmark has the highest levels of connectivity, with 92% of municipalities providing superfast broadband to at least 85% of households. In over half (59%) of all Danish municipalities, almost all (>95%) of households have access to this connection speed. The lowest levels of connectivity are found in Finland. This is particularly evident in rural municipalities where, on average, less than half of households (48%) have access to superfast broadband. Connectivity levels are also rather low in some parts of Iceland, for example, the Westfjords and several municipalities in the east. Households in urban municipalities are still more likely to have access to superfast broadband than households in rural or intermediate municipalities, but the gap appears to be closing in most. This is most evident in Norway, where the average household coverage for rural municipalities increased by 31% between 2018 and 2020. By comparison, average household coverage for urban municipalities in Norway increased by only 0.7%. In the archipelago (Åland Islands, Stockholm and Helsinki), general broadband connectivity is good; however, some islands with many second homes still have poor coverage.

- 2022 March

- Labour force

- Nordic Region

- Others